Jobless Claims Drop, But Labor Market Still Faces Challenges

#continuingclaims #initialclaims #Joblessclaims #labormarkettrends #unemploymentbenefits

Text

Photo

Don’t be surprised by #initialclaims use #alternativedata #ai #machinelearning #markets

https://www.instagram.com/p/CLcLy3rAmpO/?igshid=soeg1n2yl0y9

Photo

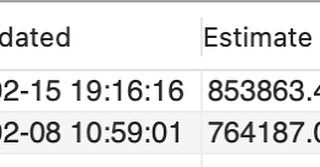

@googletrends.ig continues to be a predictor for #InitialClaims. Our number for last week was 764,187, actual release 793,000. #datascience #machinelearning #ai #finance #economics #alternativedata

https://www.instagram.com/p/CLJ30Vqg73w/?igshid=1twg62w4gn5pb

Photo

#initialclaims continues to track the predictions from our #alternativedata model based on @Google search trends. #machinelearning #ai #markets #economy

https://www.instagram.com/p/CKTzJKEgXKj/?igshid=x0fekx3r9fgt

Text

Discouraging Economic Data and Outlook from Deere This Morning

The last third quarter report for the week (still 9 companies left to report for the season) came from Deere this morning. The company blew past expectations on both the top and bottom-line, with EPS of $1.83 beating the Estimize consensus by $0.16 and the Wall Street consensus by $0.25. Revenues came in at $8.04B, well above the Estimize expectation for $7.83B and the Street’s estimate of $7.79B. Despite the third quarter beat, Deere forecast a decrease in equipment sales for the fourth quarter as lower grain prices has translated to weaker demand for tractors and agricultural machinery. The outlook sent shares down 3.5% at the open.

Additionally, there was some discouraging economic data this morning. The headline number for October Durable Goods Orders was much stronger than expected, reporting MoM growth of 0.4%, above the Estimize expectation for a 0.4% decrease. However, the core number which excludes transportation, fell 0.9% from September. While defense aircraft jumped 45.3%, non-defense aircraft orders were down 0.1%. The outlook for equipment investment also continued to moderate. Non-defense capital goods orders excluding aircraft declined 1.3%, while shipments were down 0.4%, missing the Estimize consensus for a MoM increase of 0.06%.

Initial Jobless Claims were also disappointing, reporting a weekly increase of 313,000, up 7.2% from last week, and much higher than our expectation of 286,652. This is the highest figure seen since the September 6 report showed 316,000 initial claims. This morning’s release breaks the streak of 10 consecutive weeks of claims below 300,000.

How Are We Doing?

Expectations for S&P 500 earnings growth for the third quarter stand at 11.6%. Revenues are anticipated to come in with 4.8% growth. All 10 sectors are anticipated to post positive YoY growth on both the earnings and revenue front.

Leaders

Earnings:

Energy (14.3%). Notable industry: Oil, Gas and Consumable Fuels (14.8%)

Health Care (13.9%). Notable industry: Biotechnology (45.1%)

Consumer Discretionary (13.3%). Notable industry: Internet Retailers (25.3%)

Revenues:

Health Care (12.2%). Notable industry: Biotech (39.0%).

Information Technology (7.0%). Notable industry: Software (15.8%)

Laggards

Earnings:

Utilities (2.6%). Notable industry: Gas Utilities (-8.3%).

Telecommunication Services (1.4%): All five companies are within Diversified Telecom Services. Only Verizon posted YoY growth.

Revenues:

Energy (1.1%). Notable industry: Oil, Gas and Consumable Fuels (0.4%).

Materials (2.4%). Notable industry: Paper & Forest Products (-18.3%).

Beat/Miss/Match

Earnings: With 98% of the S&P 500 reporting thus far, 56% have beaten the Estimize consensus, 34% have missed and 10% have met. This is compared to Wall Street estimates, of which 72% of companies have beat on the bottom-line, 20% have missed and 8% have met.

Revenue: 53% have beaten the Estimize consensus, 47% have missed, and 0% have met. For revenues, 60% of companies have beat the Wall Street estimate, while 40% have missed.